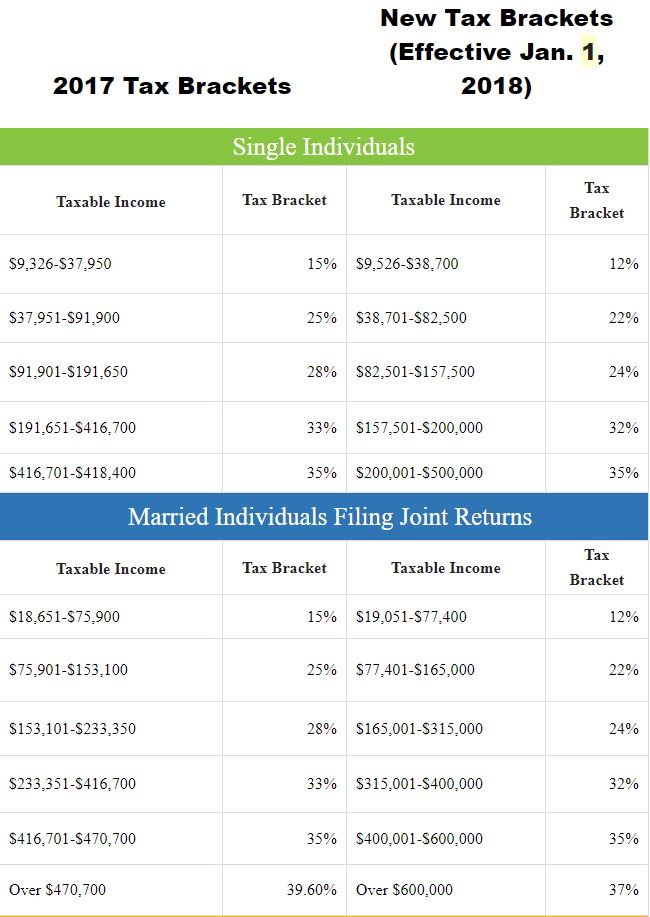

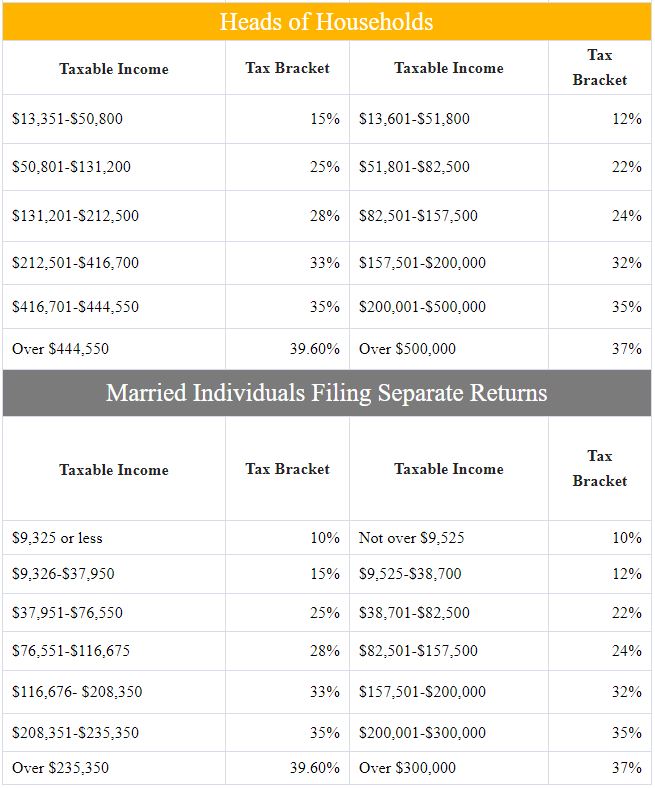

TAX CHANGES 2018 TAX REFORM

In regard to Alternative Minimum Tax, it is here to stay, however threshold has increased significantly (from $84,500 to $109,400 for married and from $54,300 to $70,300 for single) so fewer households will be effected by it.

The child tax creditdoubles to $2,000 from $1,000, also with a higher phase-out, so most will benefit from change, although you lose personal exemption deduction.

New homeowners can include mortgage interestup to $750k down from $1m and you also loose moving expense deductions.Property taxes are now combined with state incometaxes and limited to $10,000 combined deductions. This will affect many in higher property tax states, New Jersey, New York, Connecticut, Massachusetts, California, etc.

In-frequent line item changes:

Home sale gains exclusion now requires you own the home as a primary residence for five years up from 3 to exclude $250k single/$500k married.

Pass-Through Business (Schedule C) can deduct up to 20% of income.

Personal casualty or theft is only deductible in federally declared disaster situations. Still needs to exceed 10% of your adjusted gross income (AGI).

Tax deductions that won’t change:

Teacher deductionof $250 for unreimbursed expenses.

Electric car tax credit

Adoption expense up to $13,570

Student Loan Interest deduction of $2,500

From https://www.irs.gov/forms-pubs/about-form-1040 the new forms accompanying the new Form 1040 are as follows:

A general guide to what Schedule(s) you will need to file. (See the instructions for the Schedules for more information.)

IF YOU...

Have additional income, such as capital gains, unemployment compensation, prize or award money, gambling winnings. Have any deductions to claim, such as student loan interest deduction, self-employment tax, educator expenses.

THEN USE

Schedule 1IF YOU...

Owe AMT or need to make an excess advance premium tax credit repayment.

THEN USE

Schedule 2IF YOU...

Can claim a nonrefundable credit other than the child tax credit or the credit for other dependents, such as the foreign tax credit, education credits, general business credit.

THEN USE

Schedule 3IF YOU...

Owe other taxes, such as self-employment tax, household employment taxes, additional tax on IRAs or other qualified retirement plans and tax-favored accounts.

THEN USE

Schedule 4IF YOU...

Can claim a refundable credit other than the earned income credit, American opportunity credit, or additional child tax credit. Have other payments, such as an amount paid with a request for an extension to file or excess social security tax withheld.

THEN USE

Schedule 5IF YOU...

Have a foreign address or a third party designee other than your paid preparer.

THEN USE

Schedule 6TWTS Education Resources

Education Savings Bond Income Limits

You may be able to exclude all or part of the interest from qualifying Series EE or Series I bonds if you use the income for qualified educational expenses. You cannot take this benefit if your modified adjusted gross income is than $89,700 or more ($142,050 if you file jointly, or if you file as Qualifying Widow(er) with Dependent Child).

American Opportunity Tax Credit

The American Opportunity Tax Credit expanded on the Hope Credit. The income limits are higher, the credit is available for more qualified expenses, and you can use the credit for four years of post-secondary education instead of just two. In addition, you can even get a refund if you don't owe any tax for up to 40% of the credit ($1,000).

Tuition Expense Deduction

You can still deduct tuition expenses as an adjustment to income, even if you don't itemize your deductions. You generally take the tuition expense deduction if you don't qualify for an education credit or other tax break for the same expenses.

Coderdell Education Savings Accounts - Increased Limits

The new, permanent contribution limit is $2,000 per year. This benefit applies not only to higher education expenses, but also to elementary and secondary education expenses. Taxpayers with modified adjusted gross income less than $110,000 ($220,000 if filing a joint return), may be eligible to contribute to a Coverdell ESA. There are no limits on the number of separate Coverdell accounts that can be established for a beneficiary, but the total of all contributions to a single beneficiary cannot exceed $2,000 each tax year.

What is the Tax Benefit of the Coverdell ESA

Contributions to a Coverdell ESA are not deductible, but amounts deposited in the account grow tax free until distributed.

529 Plan Contributions

Many states offer tax benefits for 529 Plan Contributions however some are restricted to contributions to their individual state plan, feel free to contact me regarding such and contribution deadlines as many allow you to contribute until April 15, 2015 for the 2014 tax year.

Education Documents

2018

2018 Educational Deductions

Other

Educational Expenses PDF Document

Educational Expenses Excel Document

Email Us or call 410-860-8450